考虑碳价下限的发电商CCS投资策略与政策分析

2016-10-13 18:03张新华

管理工程学报 2016年2期

张新华, 陈 敏,叶 泽

考虑碳价下限的发电商CCS投资策略与政策分析

张新华, 陈 敏,叶 泽

(长沙理工大学经济与管理学院,湖南 长沙410114)

针对发电量与碳价双重不确定的情况,构建考虑碳价下限的发电商CCS投资期权模型,在模型解析求解基础上,通过数值仿真,考察碳价下限、政府的投资补贴、税收减免等对发电商CCS期望投资时点的影响,研究结果表明:1)若碳价下限过低,即使政府的CCS投资补贴足够高,发电商也不会进行CCS投资;2)虽然税收减免可激励发电商进行CCS投资,但“直接补贴且正常征税”可节约政府的补贴资金。

实物期权;价格下限;碳捕获与储存;电力市场

0 引言

全球气候变暖是当今人类社会所面临的最大挑战之一。在气候变暖的诸多原因中,人类活动排放的温室气体被认为是主要原因,而在温室气体引致的气候变暖效应中二氧化碳的作用高达75%以上[1]。我国是目前二氧化碳排放最多的国家,作为发展中国家,虽然暂时还没有强制的减排义务,但《京都议定书》达成的减排协议已于2012 年到期,目前世界各国都在努力推动达成新的减排协议,可以预计在不久的将来我国也将面临强制且可量化的碳减排计划。国际能源署(International Energy Agency)的调查报告认为我国的二氧化碳排放主要来源于以煤炭为主的能源行业[2]。2012年全国火力发电约37866.89478亿kWh(约占总发电量78%),按我国的碳排放量平均值约为0.8kg/kWh计算,共排放约30.29亿吨二氧化碳。因此作为碳排放主要来源之一,分析和探讨火力发电商的碳排放策略及其相关的碳排放政策,对推动低碳电力市场的建立,实现国家碳减排宏观政策的实施无疑具有重要的现实意义。

实现发电市场的碳减排,无非是以下三种途径:一是发展清洁能源,如水电、核电、太阳能与风电等,并强制现有的高排放火力发电机组退出市场;二是对现有的高排放火力机组进行技术改造,从而降低碳排放;三是对现有火力发电机组安装脱碳装置,也可实现碳减排的目标。由于目前我国火力发电机组容量占75%以上,在保证电力有效供给前提下,上述第一种途径显然是不可取的,因此实现我国发电市场的碳减排,比较现实的做法是采用上述第二、三种方法来实现。

对火力发电企业而言,碳排放具有外部性,其本身不具有经济价值,因此发电企业没有减排的积极性,但一旦政府实施碳排放许可制度,碳排放权则表现为火力发电成本的增加。目前我国的火力发电企业普通效益低下,如果在发电市场直接推广碳排放权,无疑会增加火力发电企业的负担,使本来处于市场劣势的火力发电企业处于更加不利的地位,而一旦火力发电企业长期亏损,将不可避免地带来新一轮的电力短缺。因此,在相关政策支持下,对现有火力发电机组安装CCS(Carbon Capture and Storage)设施,并实施碳排放权及其对应的交易制度,则既可给火力发电企业带来额外的收益(在一定程度内弥补火力发电企业在电能市场上的亏损),也可望实现政府的碳减排目标。

在CCS投资策略方面,文[3]较为经典,该文在对西班牙电力市场进行实证考察基础上,假定碳排放权交易价格(即碳价)服从几何布朗运动,而电价服从均值回归过程,运用实物期权方法分析了发电商的CCS投资策略,而文[4]讨论了发电成本、技术与碳价等不确定条件下的CCS 投资策略,但文[3-4]均没有考虑能源政策对CCS投资的影响。与上述研究略有不同,有部分文献考察了政策对CCS投资的影响,文[5]研究了碳规制政策不确定下,风险规制型发电商的容量投资策略;文[6]研究了碳减排不确定条件下的最化投资,并考虑了政策诱导问题;但文[5-6]构建的模型考虑的影响因素相对较少。文[7]考察了碳价下限对发电技术转换时点的影响;该文假定碳价、电价以及发电商的变动成本服从几何布朗运动,基于动态规划原理,对每一条随机样本路径进行分析,并运用LSM方法计算每一时点上的期望NPV,作为发电技术转换决策的依据。该文建立在数值仿真基础上,且假定发电商的电量是一定的,也未考虑其它政策变量对发电技术转换时点的影响。

发电商CCS投资策略由预期的投资收益决定,而投资收益无疑与其发电量(上网电量)、二氧化碳的排放权交易价格以及相关的能源政策有关;而在电力市场环境下,发电商的上网电量、碳价是不确定的。在上述文献基础上,本文针对发电商上网电量和碳价双重不确定的情况,建立考虑碳价下限的发电商CCS投资期权模型,在模型解析求解基础上,通过数值仿真考虑碳价下限、CCS投资补贴、税收政策等政策性变量对发电商CCS期望投资时点的影响,研究结果表明:1)若碳价下限过低,即使政府的CCS投资补贴足够高,发电商也不会进行CCS投资;2)税收减免可激励发电商进行CCS投资,但从节约政府的补贴资金角度来看,对发电商CCS投资进行直接补贴且正常征税(不减免)是合理的。

1 发电商CCS投资模型

影响发电商CCS投资的不确定性因素很多,其中碳排放权价格和发电商的发电量直接影响投资CCS的利润。由于碳排放权价格和发电量是随机的,因此CCS投资利润也是随机的。文[3]假定碳排放权价格服从几何布朗运动,即

(2)

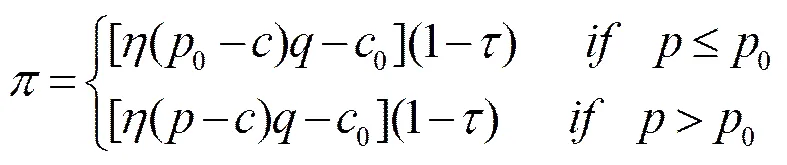

由贝尔曼方程,发电商CCS投资价值函数满足以下方程:

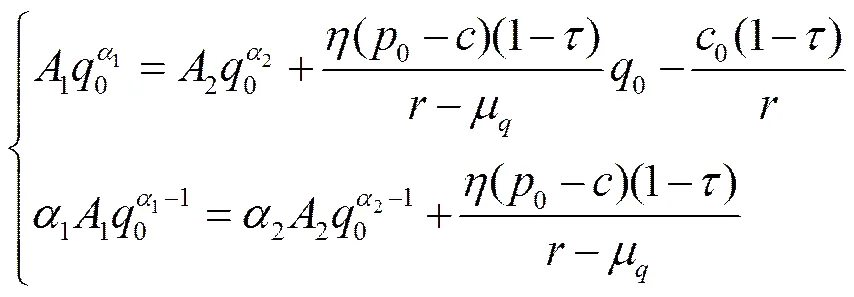

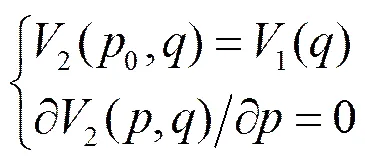

求解上式,则有:

(5)

求解上式,则有:

(6)

求解上式①,则有:

(7)

将式(5)(7)代入上式,则有:

求解上式,则有:

(9)

将式(8)代入上式,则有:

(10)

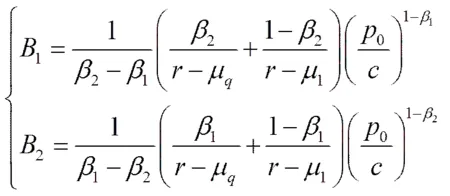

其中,

2 模型分析与数值仿真

为直观地考察发电商CCS投资阈值条件及投资时点,参照文[3],不妨设定下述参数:,。针对一台容量为60万千瓦的火力发电机组,设其CCS投资额,期间运行费为,则有:

2.1 发电商CCS投资时点的数值仿真

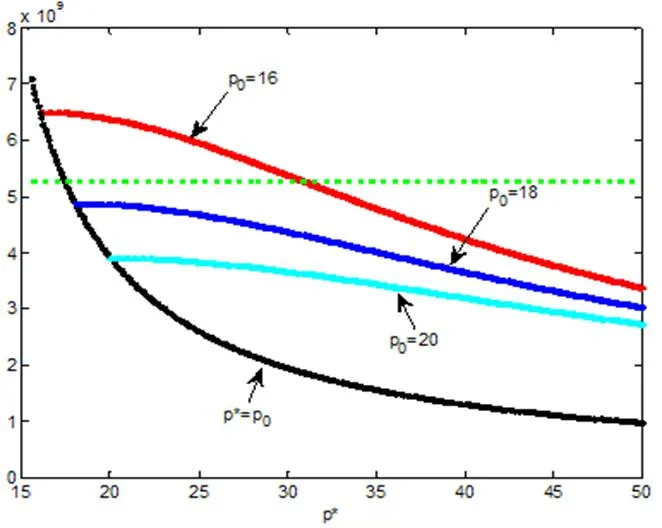

图1 发电商CCS投资阈值对应的碳价与上网电量关系

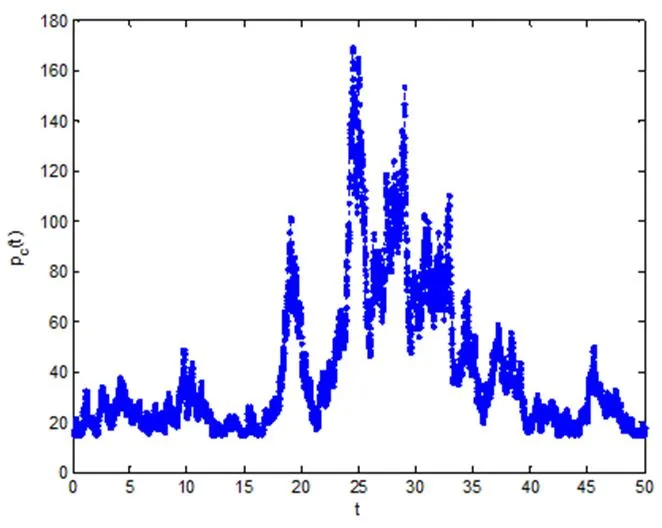

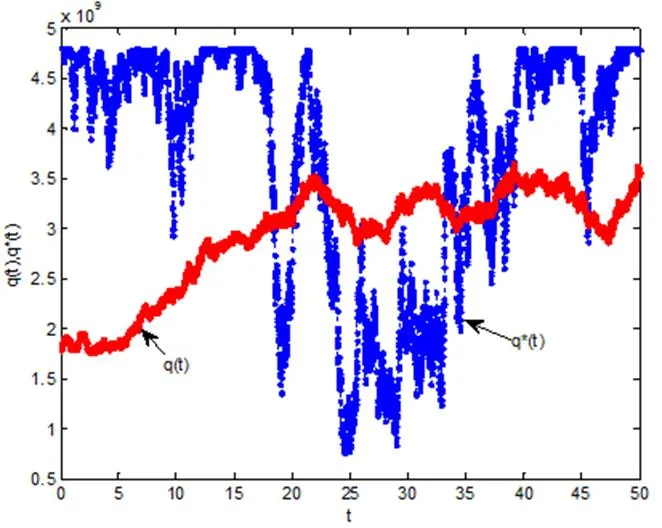

图2 一条碳价抽样路径

图1中可看出:1)随碳价下限的递增,发电商CCS投资阈值对应的上网电量递减,当时,对应的上网电量达最低;2)当碳价下限较低(如)时,投资阈值对应的上网电量将可能超过发电商的最大可供电量,显然此时发电商不会进行CCS投资。简单地,下文的数值分析中,假定碳价下限。

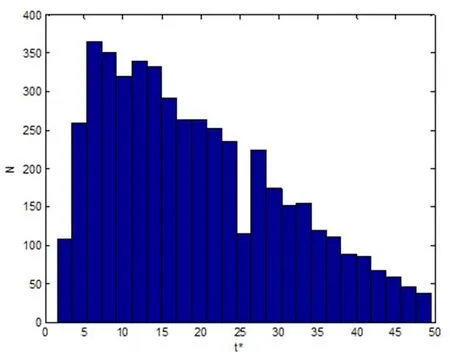

图3 基于随机抽样的CCS投资时点示意图

图4 发电商业CCS投资时点的统计柱状图

2.2发电商CCS投资的政策讨论

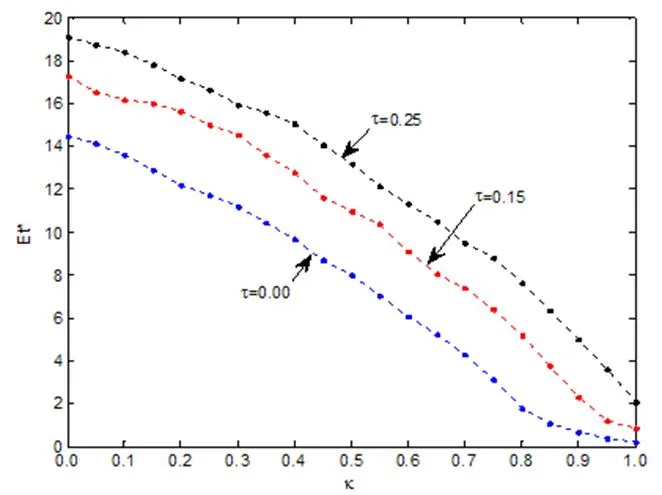

图5 投资补贴对CCS期望投资时点的影响

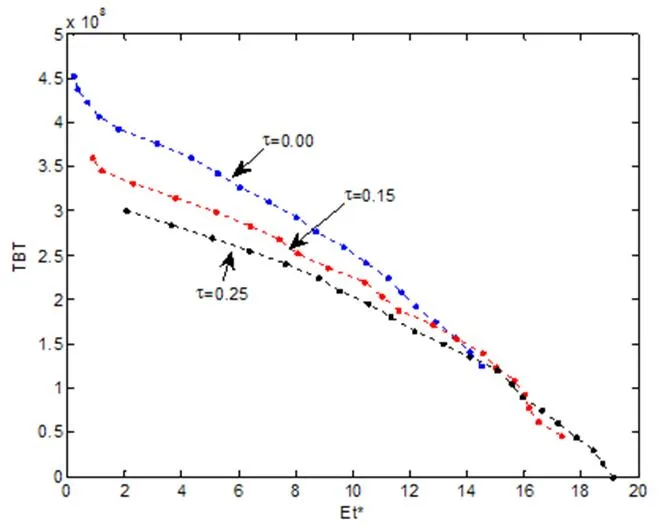

图6 不同CCS期望投资时点下的政府总补贴曲线

图7情况下的曲线

类似地,若给定发电商CCS投资期望时点,可得到类似图7的曲线。因此,对发电商CCS投资规制机构而言,在期望投资时点和碳价下限给定的前提下,不难推导出其投资补贴比率,从而实现发电市场碳减排目标。

显然,发电商CCS期望投资时点的选择,需要规制结构根据全社会总体的碳减排情况来确定,但一经确定,则可通过类似图7的分析,得到规制机构的组合规制政策;但最优的碳价下限或最优的投资补贴比率的确定,则须综合考察规制机构(如补贴资金的来源、减排目标)与其它碳排放单位(过高的碳价无疑增加了其生产或生活成本)的效用函数,本文暂不做探讨。

3 结论

随着京都议定书的到期,可以预计不久的将来我国也将面临强制且可量化的碳减排计划,作为碳排放最重要来源的火力发电企业无疑将是碳减排的重要对象,CCS投资被认为是火力发电企业碳减排最重要的途径之一。影响火力发电企业进行CCS投资的不确定性因素很多,论文针对发电量与碳价双重不确定的情况,构建考虑碳价下限的发电商CCS投资期权模型,在模型解析求解基础上,通过数值仿真考察碳价下限、政府的投资补贴、税收减免等对发电商CCS期望投资时点的影响,研究结果表明:1)若碳价下限过低,即使政府的CCS投资补贴足够高,发电商也可能不会进行CCS投资;该结论是比较直观的,如2013年上半年欧洲碳价“触底”(持续在2~5欧元/吨波动),相关的激励性政策对发电商的CCS投资几乎没有刺激作用。2)虽然执行税收减免政策能激励发电商进行CCS投资,但从节约补贴资金的角度来看,政府应直接给予CCS投资补贴,并对其投资收益正常征税;该结果与文[9]的研究结论是相吻合的(研究途径和研究对象不一样),该结论对发电商CCS投资收益“税收减免”政策的谨慎性实施提供了理论支撑。

[1] 康重庆,陈启鑫,夏清.低碳电力技术的研究展望[J].电网技术,2009,33(2):1-7.

[2] Wenji Zhou,Bing Zhu,Sabine Fuss,Jana Szolgayová,Michael Obersteiner,Weiyang Fei.Uncertainty modeling of CCS investment strategy in China’s power sector[J]. Applied Energy, 2010, 87(7):2392-2400.

[3] Luis M Abadie, José M Chamorro. European CO2prices and carbon capture investments [J].Energy Economics, 2008, 30(6):2992-3015.

[4] Lei Zhu, Ying Fan. A real options–based CCS investment evaluation model: Case study of China’s power generation sector [J].Applied Energy, 2011, 88(12):4320-4333.

[5] Lin Fan, Benjamin F Hobbs, Catherine S Norman. Risk aversion and CO2regulatory uncertainty in power generation investment: Policy and modeling implications [J].Journal of Environmental Economics and Management, 2010, 60(3):193-208.

[6] Mingxi Wang, Mingrong Wang, Shouyang Wang. Optimal investment and uncertainty on China’s carbon emission abatement [J].Energy Policy, 2012, 41(2):871-877.

[7] Alexander Brauneis, Roland Mestel, StefanPalan. Inducing low-carbon investment in the electric power industry through a price floor for emissions trading [J].Energy Policy, 2013, 53:190-204.

[8] Bockman Thor, Stein-Erik Fleten, Erik Juliussen. Investment timing and optimal capacity choice for small hydropower projects [J].European Journal of Operational Research, 2008, 190(1):255-267.

[9] Sudipto Sarkar. Attracting private investment: Tax reduction, investment subsidy, or both? [J]. Economic Modelling, 2012, 29(5):1780-1785.

Investment Strategy of CCS for Power Producer and Policy Analysis with Carbon Price Floor

ZHANG Xin-hua,CHEN Min, YE Ze

(School of Economic and Management, Changsha University of Science and Technology, Changsha 410114,China)

In the 21st century, the emissions of greenhouse gases have brought serious threats to human being’s living environment. This growing concern has made carbon emission reduction an important topic in the international community. Because power industry is the main producer of carbon dioxide, its strategy of carbon emission reduction is very important in the sustainable movement.

Carbon capture and storage (CCS) investment is a major research field about carbon emission to power producers, which contains many uncertainties, such as power demand, carbon trade price, and investment policy uncertainties. At present, most literatures model the carbon capture investment as an irreversible investment problem based on real option theory, and for simplicity, generally consider only one kind of uncertainty. Under power demand uncertainty and carbon trade price uncertainty, this paper presents an oligopoly power producer’s carbon capture investment model. This model considers carbon price floor, and investigates the impact of carbon price floor, investment subsidy and tax policy on expected investment timing based on the analysis of a numerical simulation model.

Empirical literatures on carbon trade price in Europe show that CO2trade price follows Geometric Brownian motion. Electricity power demand is assumed to follow the Geometric Brownian motion, which is proved in many studies. Based on the findings of these literatures, section II of this paper presents an oligopoly power producer’s CCS investment value function. This function considers carbon trade price floor, in which carbon trade price and power demand are variables. Applying Bellman equation and Ito’s Lemma to solve the value function, we analyze three cases and obtain three partial differential equations. By solving the value matching and smooth pasting conditions of the real option theory in carbon price floor, we can obtain analytical solutions of oligopoly power producer’s CCS investment value function, based on the solutions of above-mentioned differential equations. In addition, by comparing the values between investment and waiting to invest with classic real option method, we obtain the oligopoly power producer’s CCS investment threshold conditions: (1) invest when real power demand is higher than the threshold, or (2) do not invest when the power demand threshold is the function of carbon trade price and carbon price floor.

In section III of this paper, we use Matlab 2008 to examine numerical correlation between power demand quantity and carbon price in investment threshold with different carbon price floors based on the empirical data. In addition, we explore numerical solution of CCS investment threshold with Monte Carlo sampling method. The CCS investment threshold is stochastic due to the sample paths of two stochastic processes. In order to analyze stochastic properties of investment threshold, we sample the threshold for 5000 times, and construct histograms to examine the investment threshold’s statistical attribute. In addition, in the case of same carbon price floor the effects of policy-related investment subsidy on expected investment timing and different tax policy on total subsidy are examined. In the end, from the perspective of saving total subsidy combination strategies, including carbon price floor and subsidy, are discussed if oligopoly power producers will invest immediately.

In conclusion, power producer will not invest in CCS even if government’s subsidy is high enough when carbon price floor is too low. Tax deduction or exemption is effective to induce earlier investment. However, it is rational for government to provide power producer with investment subsidy of CCS while simultaneously taxing its future profit.

real option; price floor; CCS; power market

中文编辑:杜 健;英文编辑:Charlie C. Chen

F830.59

A

1004-6062(2016)02-0160-06

10.13587/j.cnki.jieem.2016.02.019

2013-06-30

2014-01-03

国家自然科学基金资助项目(71271033);国家社科基金重大资助项目(12&ZD051);教育部新世纪优秀人才支持计划(NCET-11-0978);湖南省高校创新平台开放资助基金(13K057)

张新华(1973—),男,湖南双峰人。长沙理工大学教授,博士(后),研究方向:能源经济管理。

① 详细求解过程见附录。

猜你喜欢

财会月刊·上半月(2022年6期)2022-06-15

中国集体经济(2020年31期)2020-11-28

中国管理科学(2020年11期)2020-03-09

北方文学(2018年18期)2018-09-14

人民周刊(2017年11期)2017-08-02

中国人口·资源与环境(2017年6期)2017-06-14

中国人口·资源与环境(2017年6期)2017-06-14

职工法律天地·下半月(2016年4期)2017-05-31

电子制作(2016年1期)2016-11-07

工业设计(2016年4期)2016-05-04